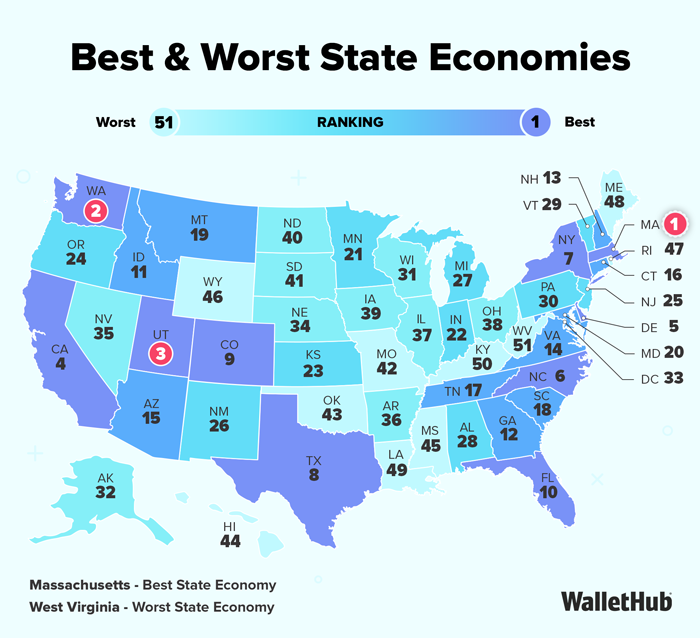

California, Texas, New York and Florida have economies so large that if they were countries, they would rank in the top 20 in the world. To determine America’s top economic performers across a variety of metrics, the personal-finance company WalletHub earlier this month released its report on 2026’s Best & Worst State Economies, as well as expert commentary.

WalletHub compared the 50 states and the District of Columbia across 28 key indicators of economic performance and strength. The data set ranges from GDP growth and the unemployment rate to startup activity and the share of jobs in high-tech industries.

Economic Performance of California (1=Best; 25=Avg.):

Overall Rank: 4th

9th – Change in GDP

26th – Exports per Capita

12th – Startup Activity

5th – % of Jobs in High-Tech Industries

25th – Change in Nonfarm Payrolls

The top five in the study were Massachusetts at number one, followed by Washington, Utah, California and Delaware. The bottom five were Rhode Island at number 47, followed by Maine, Louisiana, Kentucky and West Virginia.

“A strong state economy doesn’t guarantee success for the state’s residents, but it certainly makes financial success more attainable. Factors like a low unemployment rate and high average income help residents purchase property, pay down debt and save for the future. The best state economies also encourage growth by being friendly to new businesses and investing in new technology that will help the state deal with future challenges and become more efficient,” explained WalletHub Analyst Chip Lupo. “Massachusetts has the best state economy, and it invests a lot more in both industry and academic R&D than most other states, which leads to big payoffs in economic growth. This has led to the state having the second-most invention patents per capita. The Bay State has a lot of workers in industries that propel the economy forward, too. It has the highest share of jobs in high-tech industries, the third-highest share of STEM professionals.”

For the full report, visit: https://wallethub.com/edu/states-with-the-best-economies/21697

Expert Commentary

With Scott Thorne, Ph.D.

Instructor, Southeast Missouri State University

What are the most effective ways for state and local officials to help their local economies?

As with countries, the most effective ways for states and local officials to help local economies is to provide up to date-maintained infrastructure, a fair and unbiased legal system, good educational facilities and a transparent political system. Low taxes, while helpful, are not necessary. Witness California and New York, both high tax states but both have economies that are the envy of most low tax states.

States often compete for business investment by offering tax breaks and other incentives. Do such efforts more often result in a net positive or net negative impact on state economies? Do such efforts create a “race to the bottom” across states?

Generally, such incentives result in a net negative impact and race to the bottom as states compete to outdo each other in giving away tax dollars to organizations. Giving tax incentives to induce a sports team to come to or remain in a city, for example, has been shown to, at best, generate tax receipts equivalent to those given to the team and more often the city or state pays out more in tax incentives than the team or sports cape generates.

Where is the economy heading in 2026?

Currently, I would expect to continue to see the K-shaped economy to continue, with that part of the population with income levels allowing them to participate in the stock market continuing to do well while those not investing in the stock market will continue to see their cost-of-living increase. Unemployment should remain low but, barring a change, we will continue to see large numbers of underemployed workers. If the price of gas continues to increase at the same rate as it has over the past several weeks, we could very well tip into a recession.